SoFi Technologies (NASDAQ: SOFI)

The 2026 Equity Valuation and Strategic Outlook Report

Date: January 15, 2026

Ticker: NASDAQ: SOFI

Current Stock Price: $26.67 1

Market Capitalization: ~$36.0 Billion 2

Recommendation: Overweight / High Conviction Long

12-Month Price Target: $32.00-$36.00

In the landscape of modern financial technology, few companies have traversed the chasm from speculative disruption to profitable institutional dominance as effectively as SoFi Technologies. As of January 2026, the company stands at a pivotal inflection point, having definitively shed the volatility associated with its SPAC origins to emerge as a structural winner in the digital banking revolution. The “Compounder” thesis, long debated by bears and bulls alike, has been validated by eight consecutive quarters of GAAP profitability, a diversified revenue mix that effectively decouples growth from interest rate sensitivity, and a fortress balance sheet fortified by a strategic $1.5 billion equity raise executed from a position of strength.3

The valuation analysis presented in this comprehensive report suggests that the market is currently in the early stages of re-rating SoFi from a niche consumer lender to a diversified financial powerhouse. For years, the bear case rested on the fragility of a capital-intensive lending model and skepticism regarding the “AWS of Fintech” ambitions. By the close of 2025, these concerns have been systematically dismantled. SoFi has evolved into a top-tier financial institution with over 12.6 million members 4, demonstrating an ability to compound Tangible Book Value (TBV) at rates that eclipse legacy incumbents.

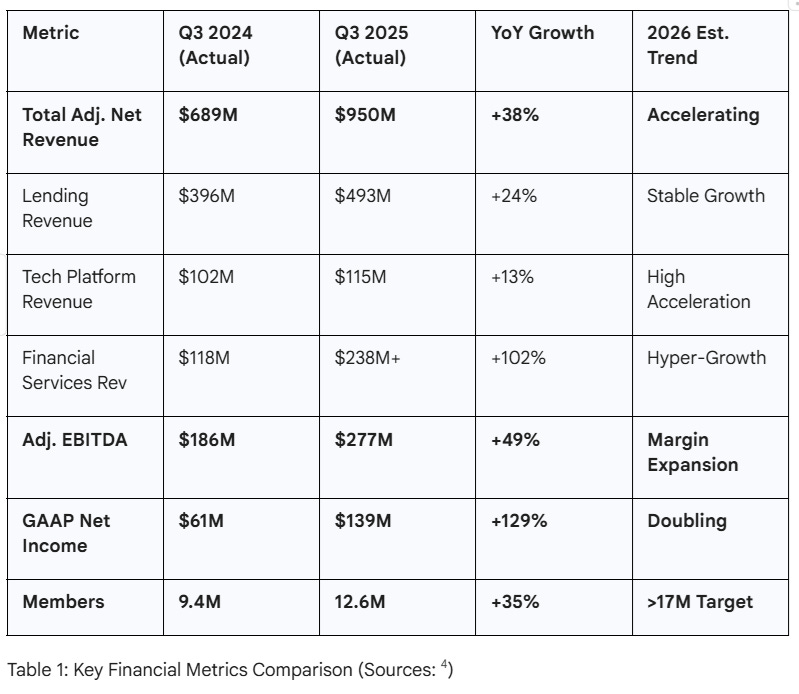

Financial performance in fiscal year 2025 shattered expectations and set a robust baseline for 2026. Third-quarter adjusted net revenue reached a record $950 million, up 38% year-over-year, while adjusted EBITDA surged 49% to $277 million.4 Crucially, the “flywheel” effect, the core of the Financial Services Productivity Loop (FSPL), is accelerating. Cross-buying behavior reached its highest level since 2022, with 40% of new products opened by existing members.5 This metric is the holy grail of fintech unit economics, driving Customer Acquisition Costs (CAC) down while extending Lifetime Value (LTV).

The recent $1.5 billion equity offering at $27.50 per share, a price level inconceivable during the lows of 2022-2024, signals an offensive strategic posture. Management intends to use this capital not to shore up weaknesses, but to accelerate growth through opportunistic M&A, technology platform expansion, and aggressive market share capture as legacy banks retrench. With earnings per share (EPS) projected to grow from an estimated $0.37 in 2025 to a management-guided range of $0.55–$0.80 in 2026 6, SoFi is positioned to deliver earnings growth exceeding 50%, a rarity in the large-cap financial sector.

This report provides an exhaustive analysis of SoFi’s valuation in 2026. It dissects the macroeconomic tailwinds, the granular performance of its three business segments, the strategic implications of its capital raise, and the valuation models that support a continued re-rating of the stock. The conclusion is unambiguous: SoFi has graduated from the “show me” phase to the “watch me” phase, emerging as the premier digital challenger bank of the decade.

2. Macroeconomic Context: The “Soft Landing” and Rate Normalization

To accurately value SoFi Technologies in 2026, one must first contextualize the operating environment, which has shifted dramatically from the restrictive policies of previous years. The “higher-for-longer” interest rate regime that strangled fintech valuations in 2023 and 2024 has given way to a normalized, yet stable, rate environment in 2025 and 2026. This shift has profound implications for SoFi’s Net Interest Margin (NIM), loan origination volumes, and the valuation multiples ascribed to growth stocks.

2.1 The Interest Rate Landscape in January 2026

As of mid-January 2026, the Effective Federal Funds Rate (EFFR) sits at approximately 3.64%.8 This represents a significant moderation from the peak rates of 2024, which exceeded 5.3%, yet it remains elevated compared to the near-zero rates of the pre-2022 era. This specific rate environment creates arguably the “Goldilocks” scenario for SoFi’s business model.

First, rates are sufficiently high to generate substantial Net Interest Income (NII) on SoFi’s growing deposit base. With deposits now exceeding $33 billion 9, SoFi benefits from the spread between the yield it generates on loans and the interest it pays to members. While SoFi pays a competitive APY to attract these deposits, its “direct deposit” customers provide a stable, lower-cost funding source compared to the warehouse facilities that financed the company in its early years. In 2024 alone, the cost of savings was approximately 220 basis points lower than warehouse facilities 10, a structural advantage that persists into 2026.

Second, the gradual decline in rates has reopened the window for refinancing. Student loan and mortgage refinancing, two of SoFi’s heritage products, were largely dormant during the peak-rate cycle as borrowers held onto legacy low rates. As the 10-year Treasury yield normalizes and mortgage rates dip, the incentive for millions of Americans to refinance existing high-rate debt accumulated during 2023-2025 increases. This serves as a potent tailwind for origination volumes in the Lending segment without requiring incremental marketing spend.

2.2 The Realization of the “Soft Landing”

The U.S. economy has largely avoided the deep recession predicted by many economists during the tightening cycle. Unemployment remains manageable, and real wage growth has turned positive. This macroeconomic resilience is critical for SoFi, whose prime borrower base, characterized by an average income exceeding $160,000 and FICO scores averaging 750 4, is historically insulated from mild economic downturns but not immune to severe recessions.

In this environment, SoFi’s credit performance has defied the broader industry trend of rising delinquencies. Net charge-offs (NCOs) for personal loans actually declined by 23 basis points to 2.60% in Q3 2025.9 This credit outperformance validates SoFi’s proprietary underwriting models and its deliberate shift up-market. While subprime lenders face rising defaults in 2026, SoFi’s strict credit box serves as a defensive moat, preserving book value and ensuring that the Lending segment remains highly profitable.

2.3 The Fintech Sector Rotation

Investor sentiment in 2026 has rotated back toward Growth-at-a-Reasonable-Price (GARP). With the “Magnificent 7” technology trade becoming increasingly crowded and valuation-stretched, institutional capital is flowing into high-growth financials that can demonstrate genuine operating leverage. SoFi’s track record of 17 consecutive quarters of meeting or beating guidance 5 has rebuilt institutional trust that was damaged during the SPAC volatility. The inclusion of SoFi in broader indices and increasing coverage by major bank analysts reflect its graduation to a “must-own” mid-cap financial stock. The market is no longer pricing SoFi solely on revenue multiples but is increasingly respecting its earnings power and book value growth.

3. Financial Performance Analysis: The Profitability Inflection

SoFi’s fiscal year 2025 performance serves as the foundational bedrock for the 2026 valuation thesis. The numbers tell a compelling story of a business that has successfully scaled past its fixed cost base and is now enjoying the benefits of significant operating leverage. The transition from a company burning cash to gain market share to one generating cash while gaining market share is complete.

3.1 Revenue Velocity and Strategic Diversification

In Q3 2025, SoFi reported adjusted net revenue of $950 million, a 38% increase year-over-year.4 This growth is not monolithic; it is distributed across three distinct but reinforcing segments, reducing the company’s reliance on any single revenue stream.

The most critical trend within this data is the decisive shift toward non-lending revenue. In Q3 2025, the combined Financial Services and Technology Platform segments generated $534 million, representing 56% of total adjusted net revenue.5 This is a watershed moment for the valuation thesis. For years, critics labeled SoFi a “bank masquerading as a tech company” to justify a lower valuation multiple. Now, with over half of its revenue derived from fee-based, capital-light sources, the argument for a “tech multiple” is mathematically justified. The revenue mix has structurally shifted, providing greater predictability and lower capital intensity.

3.2 Profitability and The “Rule of 40”

SoFi has achieved eight consecutive quarters of GAAP profitability as of Q3 2025.4 The quality of this earnings growth is high, with Q3 Net Income of $139 million representing a 14% net income margin.9 This is not “adjusted” profitability heavily reliant on adding back stock-based compensation; this is true bottom-line income available to shareholders.

Management frequently cites the “Rule of 40” (Revenue Growth % + EBITDA Margin %) as a benchmark for high-quality growth companies. In Q3 2025, SoFi achieved a score of 67 (38% growth + 29% EBITDA margin).4 This places SoFi in the top decile of all publicly traded software and fintech companies, significantly outperforming peers like PayPal, Block, and Affirm on this efficiency metric. This sustained efficiency demonstrates that SoFi does not need to burn cash to grow; it generates substantial cash flow while growing at a rapid clip.

3.3 Balance Sheet Strength and Tangible Book Value Growth

A key, often overlooked, valuation driver is the rapid accumulation of Tangible Book Value (TBV). TBV grew by $1.9 billion in Q3 2025 alone, ending the period at $7.2 billion, or approximately $7.29 per share.4 Over the past two years, SoFi has more than doubled its TBV.5

In the banking sector, stocks typically trade at a multiple of TBV. High-quality banks with high Return on Equity (ROE) often trade at 2.0x to 2.5x TBV. At a stock price of ~$27, SoFi trades at roughly 3.7x TBV. While this appears rich for a traditional bank, it is inexpensive for a technology platform growing revenue at 38%. The convergence of book value growth and earnings growth creates a significant “margin of safety” for investors. Even if the technology premium were to evaporate entirely, the fundamental banking value is rapidly catching up to the share price, providing a solid floor for the stock.

4. Strategic Analysis: The Financial Services Productivity Loop (FSPL)

The true “moat” of SoFi’s business model is the Financial Services Productivity Loop (FSPL). This strategy is not merely a marketing tagline; it is a structural economic advantage derived from the integration of disparate financial products into a single, cohesive application experience. This integration drives cross-selling, data synergies, and superior unit economics.

4.1 The Unit Economics of the “One-Stop Shop”

The FSPL creates a virtuous cycle of acquisition, engagement, cross-sell, and retention. The mechanism functions as follows:

Acquisition: A user typically joins SoFi for a high-yield savings account (SoFi Money) or a credit card (SoFi Credit Card). The Customer Acquisition Cost (CAC) for these products is relatively low compared to the high CAC associated with acquiring a personal loan customer on the open market.

Engagement: The user connects their external accounts via SoFi Relay, a financial insights tool. This gives SoFi a window into the user’s entire financial life, including competitor loans and spending habits.

Cross-Sell: SoFi’s data engine identifies opportunities, such as a user paying 22% interest on a competitor’s credit card. It then offers a pre-approved Personal Loan or Student Loan Refi to consolidate that debt.

Monetization: Because the user is already in the ecosystem, the CAC for this second, high-margin product is near zero.

Retention: A user with a checking account, a credit card, and a loan is statistically far less likely to churn than a single-product user.

In Q3 2025, this strategy resulted in 40% of all new products being opened by existing members.5 This metric is arguably the strongest indicator of the FSPL’s health. It implies that nearly half of SoFi’s sales growth comes with negligible marketing cost, boosting contribution margins and creating a compounding effect on profitability.

4.2 Member Growth Trajectory

Membership grew 35% year-over-year to 12.6 million in Q3 2025.4 Analyst projections and management commentary suggest a target of 17.2 million members by the end of 2026.11 This growth is fueled by aggressive marketing partnerships (such as the NBA and NFL affiliations) and continuous product innovation.

If SoFi reaches 17 million members, it will have captured approximately 5-6% of the U.S. adult population. However, the runway for “share of wallet” expansion remains vast. Currently, the average products per member is roughly 1.5.4 Increasing this ratio to 2.0 or 3.0 represents a massive revenue opportunity without adding a single new member. The launch of new products like the Smart Card and expanded investment options is directly aimed at increasing this ratio.

5. Segment Deep Dive: Lending, Tech Platform, & Financial Services

To properly value SoFi, one must value the sum of its parts, as each segment operates with distinct economics, growth drivers, and competitive dynamics.

5.1 Lending: The Cash Cow Reimagined

Revenue (Q3 2025): $493M (+24% YoY) 4

Contribution Margin: ~54%

Key Insight: The Shift to “Capital Light” via the Loan Platform Business.

Historically, SoFi held loans on its balance sheet to collect interest income, exposing the company to credit risk and capital constraints. In 2024 and 2025, SoFi pivoted aggressively to a Loan Platform Business (LPB) model. In this model, SoFi originates loans on behalf of third parties, such as asset managers and regional banks, for a fee, without ever holding the asset on its own balance sheet.

In Q3 2025, the LPB generated $167.9 million in fee-based revenue, up 29% sequentially and 2.75x from the prior year.4 This strategy transforms lending from a lumpy, capital-intensive business into a recurring, high-ROE fee stream. It effectively decouples revenue growth from balance sheet risk, allowing SoFi to scale origination volumes significantly higher than its own capital base would otherwise permit.

2026 Outlook for Lending:

Personal Loans: SoFi continues to dominate the “prime” unsecured market. The credit quality remains pristine, with FICO scores of new borrowers averaging ~745-750.

Student Loans: A renaissance in refinancing is expected as interest rates drop. While political uncertainty around forgiveness persists, the private refinancing market for high-income earners (e.g., medical and law graduates) remains robust.

Home Loans: Management expects an “excellent year” in 2026 for the mortgage business as rates stabilize.11

Credit Quality: The deliberate focus on high-FICO borrowers acts as a natural hedge against economic volatility.

5.2 Technology Platform (Galileo & Technisys): The “AWS of Fintech”

Revenue (Q3 2025): $115M (+13% YoY, accelerating) 4

Accounts: ~160 Million

Key Insight: The 2026 Acceleration.

This segment has historically been the laggard in terms of growth rate (10-15%) compared to the rest of the business, leading to investor frustration. However, CEO Anthony Noto has explicitly flagged 2026 as a “year of accelerating growth” for the Tech Platform.12

The thesis for acceleration rests on several pillars:

Legacy Core Migration: Large banks are finally moving to upgrade their 40-year-old COBOL-based core systems. Technisys (SoFi’s core banking platform) and Galileo (issuer processing) offer a modern, cloud-native alternative. Sales cycles for these enterprise deals are long (18-24 months), and deals signed in 2024 are starting to go live in 2026.

New Strategic Clients: Noto referenced upcoming launches with a “large financial retail company” and a “government direct express benefit” program in 2026.12 These are volume-heavy contracts that provide a step-function increase in processed transactions.

Government & B2B: Expansion into government payments and B2B lending creates new, massive Total Addressable Markets (TAMs) beyond consumer fintech.

If the Tech Platform accelerates to 20-25% growth in 2026 as predicted, it will likely trigger a significant multiple re-rating. Investors will begin to value this segment like a high-growth SaaS business (10x-15x Sales) rather than a lower-multiple service provider.

5.3 Financial Services: The Hyper-Growth Engine

Revenue (Q3 2025): $238M+ (+102% YoY) 4

Key Products: SoFi Money, Invest, Credit Card, Relay.

Key Insight: Extreme Operating Leverage.

This segment was loss-making for years but turned profitable in 2024. In 2025, it became a primary driver of bottom-line growth. The contribution margin is expanding rapidly as revenue doubles while fixed costs remain relatively flat, demonstrating the classic software-like scalability of the platform.

2026 Drivers:

SoFi Invest: The relaunch of crypto trading and the introduction of alternative assets (such as private equity and commodities) are expected to drive significant trading volumes.13

SoFi Money: Deposit growth lowers the company’s overall Cost of Funding. By replacing high-cost warehouse debt with lower-cost member deposits, SoFi directly boosts the NIM of the Lending business.

Smart Card: The new “Smart Card” integrates checking, savings, and credit into a single form factor, reducing friction and increasing daily active usage. This product is designed to create “lock-in” and ensure SoFi becomes the primary transactional account for its members.14

6. The $1.5 Billion Capital Raise: A Strategic War Chest

In December 2025 and January 2026, SoFi executed a public offering of approximately 54.5 million shares at $27.50 per share, raising roughly $1.5 billion in gross proceeds.3 The market initially reacted with volatility due to dilution fears, but the stock quickly stabilized near the offering price.

Strategic Rationale: Why Raise Capital When Profitable?

Critics argued the raise was unnecessary given SoFi’s robust profitability. However, viewed strategically, this move represents a proactive fortification of the business:

Capitalizing on Strength: Raising equity at ~$27.50 (near 52-week highs) is significantly less dilutive than raising capital at $5.00 (the 2022 lows). It allows the company to bolster its balance sheet with minimal impact on existing shareholders.

M&A Firepower: The fintech sector is ripe for consolidation. Many “Zombie Fintechs” possess excellent technology or user bases but lack sustainable business models and are trading at distressed valuations. SoFi can now use this capital to acquire niche players (e.g., in wealth management, payments, or insurance) to plug gaps in the FSPL.

Balance Sheet Fortress: With Basel III “Endgame” regulations looming for larger banks, having excess capital ratios allows SoFi to continue growing its loan book aggressively while competitors are forced to pull back. It also provides the flexibility to warehouse more loans if the LPB market temporarily freezes due to macro volatility.

Debt Optimization: Snippets suggest SoFi successfully exchanged high-cost convertible debt for equity, effectively deleveraging the company and removing interest expense, which boosts future EPS.16

The dilution (~4-5%) is a small price to pay for the strategic optionality this cash pile provides. It signals that management is playing offense for the next decade, focusing on long-term dominance rather than short-term metrics.

7. Product Innovation: The 2026 Roadmap

SoFi’s valuation is partially supported by its relentless pace of product innovation. 2026 promises several major launches that differentiate it from commoditized neobanks and legacy institutions.

7.1 SoFi Pay & Stablecoin (SoFi USD)

SoFi is leveraging its bank charter and technology capabilities to launch SoFi Pay and a fully reserved Stablecoin.5

The Thesis: Payment rails are expensive, with Visa and Mastercard interchange fees eating into margins. By creating a closed-loop payment system via a stablecoin, SoFi can facilitate instant, near-zero cost transfers for members, especially for cross-border remittances (starting with Mexico).5

Regulatory Advantage: As a regulated bank, a SoFi-issued stablecoin carries a level of trust and compliance that issuers like Tether or Circle cannot match for institutional clients. This could become a massive B2B revenue stream for the Tech Platform, positioning SoFi as a bridge between traditional finance (TradFi) and decentralized finance (DeFi).

7.2 The “Smart Card”

Launched in late 2025, the Smart Card consolidates debit and credit functionality. It automatically pays off the credit balance from the high-yield savings account, optimizing the user’s cash management without manual intervention. This product creates significant “lock-in” and ensures SoFi becomes the primary transactional account.14 By automating the “pay off in full” behavior, SoFi attracts the most credit-worthy users who transact frequently but carry low risk.

7.3 AI Integration (SoFi Coach)

SoFi is integrating Generative AI into its SoFi Coach product. Unlike generic chatbots, this AI has access to the user’s transaction data via Relay. It can proactively suggest actionable financial moves: “You are spending $400/month on subscriptions you don’t use, click here to cancel” or “Moving $5k from checking to savings will earn you $200 more this year.” This hyper-personalization increases engagement, builds trust, and drives cross-sell conversion rates.14

8. Valuation Models and Price Targets

Valuing SoFi is complex because it is a hybrid entity. It is part bank (lending), part SaaS (Galileo), and part consumer tech (app). Therefore, a multi-faceted valuation approach is required.

8.1 Sum-of-the-Parts (SOTP) Valuation

A SOTP approach is arguably the most accurate way to value SoFi, as it respects the distinct multiples applicable to each segment.

Note: This conservative SOTP lags the current Market Cap.

Critique of SOTP: The conservative SOTP yields a value (~$22B) lower than the current market cap ($36B). This suggests the market is pricing in significant future growth or assigning a higher “platform premium” to the integrated ecosystem (the “Whole is greater than sum of parts”). The market is effectively valuing SoFi on 2027/2028 numbers, anticipating that the compound growth will continue unabated.

8.2 Earnings Power Valuation (Forward P/E)

A Forward P/E analysis provides a clearer picture of the growth premium.

2026 EPS Est: $0.55 - $0.80 (Bull Case / Mgmt Guidance).6

Current Price: $27.00.

Implied P/E:

At $0.55 EPS: ~49x P/E.

At $0.80 EPS: ~33x P/E.

For a company growing revenue at 30%+ and earnings at 50-100%, a PEG ratio (Price/Earnings-to-Growth) of 1.0 is considered fair value.

**Sanity Check: If SoFi grows earnings 80% in 2026, a 49x multiple implies a PEG well < 1.0, suggesting the stock is undervalued relative to its growth rate.

Applying a conservative “Fintech Compounder” multiple of 42x to the upper end of 2026 EPS ($0.80) yields an implied year-end 2026 value of $34.00, representing an ~25% annual return from current levels.

Looking into 2027, assuming EPS growth moderates to ~40% (to ~$1.12), a 35x multiple implies a value of $39.20, equating to a ~20% two-year CAGR from today’s price.

8.3 The “Trillion Dollar” Ambition

CEO Anthony Noto has stated an ambition to become a top 10 financial institution.18 While a trillion-dollar market cap is a distant aspiration, achieving “Top 10” status implies a valuation in the hundreds of billions.

Top 10 Bank Market Cap Threshold: ~$80-100 Billion (e.g., U.S. Bancorp, Citigroup).

For SoFi to reach a $100 Billion market cap (approx. $75/share), it needs to roughly triple its current size. Given the 30-40% compounding growth rate, this is mathematically achievable within 4-5 years (by 2030), provided execution remains flawless.

Price Target Justification:

Base Case (12-month): $35.00. Based on successful execution of 2026 guidance, 30% revenue growth, and stable rates.

Bull Case (12-month): $42.00 - $45.00. Assumes Tech Platform re-acceleration beats estimates, crypto revenue surges, and EPS hits the high end of guidance ($0.80).

Bear Case (12-month): $20.00. Assumes a recession spikes credit losses, forcing a pullback in lending, or Tech Platform growth stagnates.

9. Risks to the Thesis

Despite the bullish outlook, significant risks remain that investors must monitor closely.

Execution Risk on Tech Platform: The “acceleration” promised for 2026 must materialize. If growth remains stuck at 10-12%, the market will likely strip away the tech multiple, re-rating SoFi closer to a traditional bank (10x-12x Earnings), which would crush the stock price to the low teens.

Credit Cycle Deterioration: While SoFi’s borrower base is prime, a “white-collar recession” (impacting tech/finance jobs) could disproportionately hurt their specific demographic. Rising unemployment among high-earners would spike charge-offs and erode profitability.

Regulatory Interventions: The CFPB or OCC could crack down on “Bank-Fintech” partnerships or impose stricter capital requirements on digital banks. Additionally, crypto regulations remain fluid; a crackdown on stablecoins could stifle the SoFi Pay initiative before it gains traction.

Dilution Fatigue: While the $1.5B raise was strategic, investors are weary of share count expansion (Stock-Based Compensation + Offerings). Continued dilution without commensurate EPS growth will alienate institutional holders.

Valuation Compression: If market sentiment shifts back to “risk-off,” high-multiple stocks are the first to be sold. SoFi at 40x earnings is vulnerable to multiple compression even if the underlying business performs well.

10. Conclusion: The Premier Fintech Holding of the Cycle

SoFi Technologies in 2026 is a fundamentally different entity than the SPAC-era company of 2021. It has survived the crucible of rising rates, proven the resilience of its credit models, and achieved the elusive goal of GAAP profitability at scale.

The data presented in this report, record revenue, expanding margins, diversified income streams, and a fortified balance sheet, supports the conclusion that SoFi is a long-term compounder. The FSPL is working, creating a competitive moat that legacy banks struggle to replicate due to their siloed technology and branch-heavy cost structures.

The current valuation, while demanding in terms of P/E, is justified by the hyper-growth trajectory of the bottom line and the strategic optionality provided by the recent capital raise. SoFi is essentially “fully funded” to chase its aggressive growth targets for the remainder of the decade.

For investors with a multi-year time horizon, SoFi represents a rare opportunity to own a generational disruptor in the early innings of its profitability phase. The volatility is the price of admission, but the compounding engine is now firing on all cylinders.

Final Verdict: The “Compounder” thesis is intact. SoFi is a High Conviction Long, with a clear path to $34.00 in the next 12 months as the 2026 earnings story unfolds.

Works cited

SoFi Technologies, Inc. (SOFI) - Stock Information, accessed January 15, 2026, https://investors.sofi.com/stock-information/default.aspx

SoFi Technologies Reports Net Revenue of $697 Million and Net Income of $61 Million for Q3 2024, Demonstrating Durable Growth and Strong Returns, accessed January 15, 2026, https://www.sofi.com/press/sofi-technologies-reports-net-revenue-697-million-net-income-61-million-q3-2024-demonstrating-durable-growth-strong-returns/

SoFi Technologies, Inc. Announces Pricing of Public Offering of Common Stock, accessed January 15, 2026, https://fintech-pulse.com/news/sofi-technologies-inc-announces-pricing-of-public-offering-of-common-stock/

SoFi Reports Third Quarter 2025 with Record Net Revenue of $962 Million, Record Member and Product Growth, Net Income of $139 Million - (SOFI) - Investor Relations, accessed January 15, 2026, https://investors.sofi.com/news/news-details/2025/SoFi-Reports-Third-Quarter-2025-with-Record-Net-Revenue-of-962-Million-Record-Member-and-Product-Growth-Net-Income-of-139-Million/default.aspx

SoFi Q3 2025 Earnings Transcript_FINAL.docx, accessed January 15, 2026, https://s27.q4cdn.com/749715820/files/doc_financials/2025/q3/SoFi-Q3-2025-Earnings-Transcript_FINAL.pdf

‘Don’t Pull the Trigger Just Yet,’ Says Deutsche Bank About SoFi Stock | Nasdaq, accessed January 15, 2026, https://www.nasdaq.com/articles/dont-pull-trigger-just-yet-says-deutsche-bank-about-sofi-stock

Is SoFi a Buy, Sell, or Hold in 2026? | The Motley Fool, accessed January 15, 2026, https://www.fool.com/investing/2025/12/16/is-sofi-a-buy-sell-or-hold-in-2026/

Effective Federal Funds Rate (EFFR) | FRED | St. Louis Fed, accessed January 15, 2026, https://fred.stlouisfed.org/series/EFFR

2025 Q3 Investor Presentation, accessed January 15, 2026, https://s27.q4cdn.com/749715820/files/doc_financials/2025/q3/2025-Q3-Investor-Presentation-v_Final.pdf

SoFi Technologies Reports Net Revenue of $697 Million and Net Income of $61 Million for Q3 2024, Demonstrating Durable Growth and Strong Returns, accessed January 15, 2026, https://s27.q4cdn.com/749715820/files/doc_financials/2024/q3/Q3-2024-Earnings-Release.pdf

I Made 3 Accurate Predictions About SoFi in 2025. Here Are 3 More Bold Predictions for 2026. | Nasdaq, accessed January 15, 2026, https://www.nasdaq.com/articles/i-made-3-accurate-predictions-about-sofi-2025-here-are-3-more-bold-predictions-2026

SoFi CEO on earnings: EPS lower due to long-term investment in business over near-term profit - YouTube, accessed January 15, 2026,

SoFi at JPMorgan Conference: Strategic Growth and Challenges - Investing.com, accessed January 15, 2026, https://www.investing.com/news/transcripts/sofi-at-jpmorgan-conference-strategic-growth-and-challenges-93CH-4045975

SOFI Stock Rises 40% in Half a Year: Play or Time to Pause? - January 7, 2026 - Zacks.com, accessed January 15, 2026, https://www.zacks.com/stock/news/2813748/sofi-stock-rises-40-in-half-a-year-play-or-time-to-pause

SoFi Technologies completes sale of 57.8 million shares in public offering - Investing.com, accessed January 15, 2026, https://www.investing.com/news/sec-filings/sofi-technologies-completes-sale-of-578-million-shares-in-public-offering-93CH-4431131

SoFi Announces $1.5 Billion Public Offering, Stock Falls Over 6% - Alpha Spread, accessed January 15, 2026, https://www.alphaspread.com/market-news/stock-movements/sofi-announces-15-billion-public-offering-stock-falls-over-6

SoFi Technologies, Inc. (SOFI) - Investor Relations, accessed January 15, 2026, https://investors.sofi.com/overview/default.aspx

SoFi’s CEO Believes It Could Become a Trillion-Dollar Company. Could It Actually Happen?, accessed January 15, 2026, https://www.nasdaq.com/articles/sofis-ceo-believes-it-could-become-trillion-dollar-company-could-it-actually-happen